Menu

Tax appointments can bring up a lot of emotions. For many people, taxes feel personal. They reflect income, family changes, debt, and significant life decisions from the past year. It’s normal to worry about missing paperwork or forgetting something important. The good news is that most tax appointments follow a familiar pattern, and the information needed is pretty consistent from one preparer to the next.

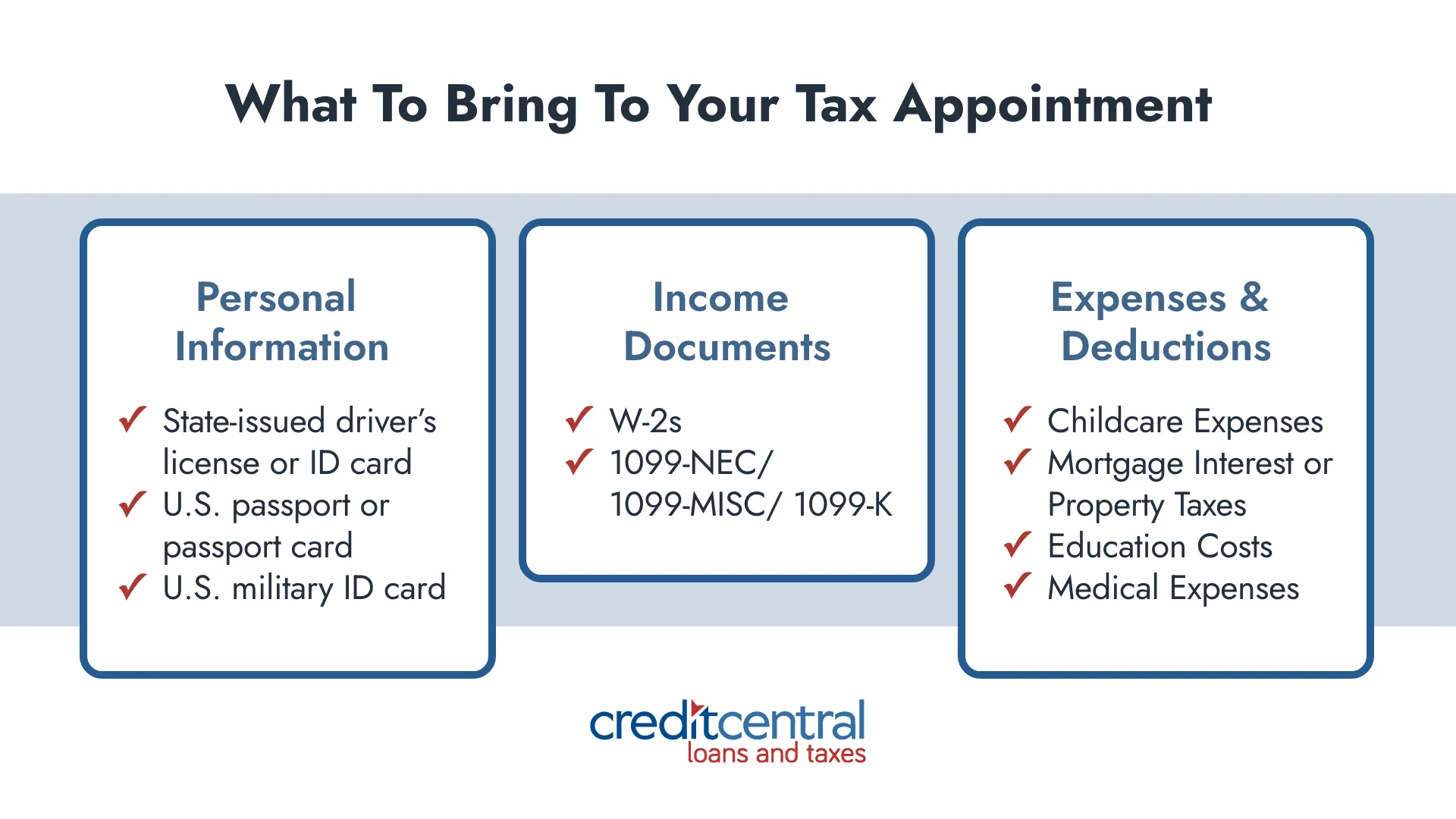

Whether you work with a national tax office, a local professional, or a tax preparation service like Credit Central, gathering documents in advance can make the process feel more manageable. Preparation helps the appointment move at a comfortable pace and gives your preparer a clearer picture of your situation. It also reduces the chance of follow-up requests later. The sections below break down what to bring and why each item matters, so you can walk into your appointment feeling ready rather than overwhelmed.

Personal information forms the foundation of every tax return. These details confirm who you are, who is included on your return, and how the IRS matches your filing to its records. Even if nothing has changed since last year, it’s still important to have this information available.

A valid photo ID helps confirm your identity and protects against fraud. Many tax preparers require an ID with a photo before filing, especially if you are a new client. Bringing it to your appointment can prevent delays and help the process move forward smoothly.

What type of ID is considered government-issued? Here is a list of acceptable forms of identification for tax purposes.

Social Security numbers are required for everyone listed on the return. This includes children and other dependents. Having cards or official records helps avoid errors that can slow processing.

Last year’s return provides helpful context. It shows filing status, carryover credits, and prior deductions. Your preparer may refer to it when reviewing changes or answering questions.

Income reporting is one of the most important parts of tax filing. It’s super important to understand where all of your income is coming from and to have the documentation to support it. Failing to report income can cause problems later.

Be sure to bring every document that shows money earned during 2025. Even smaller income sources matter.

W-2 forms report wages from employers who withheld taxes throughout the year. Employers are required to provide W-2s by January 31 for the prior employment year. If you worked multiple jobs, bring a W-2 from each employer, since missing even one can affect your totals.

These forms report non-employee income, payments, or transactions. Freelancers, contractors, and gig workers often receive them. Some platforms issue summaries instead of traditional forms, which can also be used.

Unemployment benefits are taxable income. If you received benefits during 2025, bring the statement showing total payments. This income must be reported even if taxes were withheld.

Retirees may receive forms showing Social Security benefits or retirement distributions. These documents help determine how much, if any, of that income is taxable.

Not everyone claims deductions beyond the standard amount, but if you do, documentation matters. These records help support credits and deductions tied to specific expenses paid during the year.

If you paid for childcare to work or attend school, bring records showing childcare provider details and amounts paid. This information may support childcare-related credits.

Tuition statements, student loan interest forms, and education-related receipts can affect eligibility for education credits. These items are helpful for students and parents alike.

Out-of-pocket medical costs may be relevant in certain situations. Bring summaries or receipts if medical expenses were high during the year.

Homeowners should bring statements showing mortgage interest paid and property taxes. These documents are commonly used when itemizing deductions.

Self-employed workers should bring expense records such as mileage logs, supply costs, and home office details. Clear records help explain income and reduce confusion.

Some documents don’t fit neatly into income or deduction categories but still play an essential role during tax preparation. Bringing these items can help your preparer complete the return more efficiently.

Providing bank routing and account numbers allows refunds to be deposited directly. This method is often faster than receiving a paper check.

If you received letters or notices from the IRS, bring them to your appointment. These documents often include reference numbers or instructions that affect filing.

For many people, the most challenging part of filing taxes is not the paperwork itself, but the uncertainty around what actually happens during an appointment. Not knowing what questions will be asked or how decisions are made can cause hesitation. The tax prep process is more structured than it may seem, and most appointments follow a predictable flow.

Understanding each step ahead of time can help you feel more at ease and better prepared to participate in the conversation. While tools and timelines may vary slightly by provider, the core steps below are consistent across most tax preparation services and apply no matter who prepares your return.

As an additional note, if more time is needed, a tax extension may be an option. An extension allows extra time to file, but not extra time to pay. A tax preparer can explain whether this makes sense and what steps are required.

The process usually begins with an intake conversation and a review of your documents. This is where your preparer gathers background details and checks that the required forms are present. It is also the point where gaps are identified early, before filing begins. The goal is clarity, not perfection.

Credit Central provides tax preparation services designed to meet people where they are, whether filing feels familiar or overwhelming. One helpful option is a free estimate, which gives you a clearer picture of a potential refund before moving forward. When you are due a refund, there are no upfront fees for tax preparation. Instead, you can choose to have the preparation cost deducted directly from your refund after the IRS processes your return.

For those who want access to funds sooner, Credit Central also offers tax refund advances up to $7,500, based on eligibility. This option allows qualified filers to receive part of their expected refund before the tax season wait is over.

Getting started is easy. Use the tax branch locator on the Credit Central website to find the nearest location and schedule a time with a local team member who can walk you through the next steps.

Here are some common questions that come up during intake:

“Did anything change in your household or income last year?”

Changes like a new job, added dependents, or a move can affect filing status and credits. Even changes that seem small may matter. Your preparer asks this to understand how 2025 compares to prior years and whether additional forms or explanations are needed.

“Do you have income beyond your W-2?”

This question helps uncover freelance work, side income, or interest that may not be obvious at first glance. Income does not always come with a traditional tax form, so this discussion helps confirm that all earnings are accounted for.

“Have you received any letters from the IRS?”

IRS letters often relate to prior filings, identity verification, or balance questions. Bringing them up early allows the preparer to address issues before submitting a new return and avoids unnecessary delays.

Once income is confirmed, the next step is reviewing possible credits and deductions. These two concepts often get confused, but they work differently.

A tax deduction reduces the amount of income that is taxed. Common deductions include student loan interest, certain medical expenses, or business costs for self-employed filers.

A tax credit directly reduces the tax owed. Credits can have a larger impact because they apply dollar for dollar. Examples include education credits and child-related credits.

Your preparer reviews eligibility, explains what applies to your situation, and confirms that documentation supports each item. This part of the process is about accuracy and proper reporting rather than chasing outcomes.

After credits and deductions are applied, your preparer calculates the result. This is when you learn whether you are due a refund or have a balance due.

Refunds are common but not guaranteed. A refund simply means more tax was paid during the year than was owed. A balance due means withholding or estimated payments did not fully cover the tax bill. Neither outcome is a judgment or a mistake by itself.

Your preparer should walk through the numbers and explain how income, withholding, and credits led to the final result. Understanding this step helps reduce surprises in future years.

Once everything is reviewed and approved, the return is submitted electronically. E-filing is now the standard method for federal returns and is faster than mailing paper forms.

After submission, you receive confirmation that the return was accepted. This confirmation is important. It shows that the return passed initial checks and is in the system. Your preparer should explain how to keep a copy of your return and where to find confirmation details if you need them later.

Refund timing is one of the most common questions during tax season. According to the Internal Revenue Service, most federal refunds are issued within 21 calendar days. Filing electronically and choosing direct deposit is the fastest combination. Taxpayers who use both typically receive refunds within 3 weeks.

This timeline applies only to federal returns. State refund timelines vary and may take longer depending on the state and time of year. Your preparer can explain what to expect for both and how to track progress once filing is complete.

The tax prep process is not meant to feel intimidating. It is a series of steps designed to collect information, apply rules correctly, and submit a complete return. Asking questions is part of the process, not a sign that something is wrong.

Understanding what happens at each stage can ease hesitation and help you approach your appointment with a clearer mindset. When you know what to expect, tax filing becomes a task you move through, not something you put off year after year.

Taxes often come with expectations, especially around refunds. Some people count on them each year, while others worry about owing money. The reality is that outcomes can change from one year to the next, even if your income feels similar. Understanding why refunds vary, how timing works, and what options exist if you owe money can help set realistic expectations for the 2026 filing season.

Refunds are not bonuses or rewards. They reflect how much tax was paid during the year compared to what was actually owed. Changes in income, withholding, tax credits, or life events like a new job or a dependent can all affect the final number. Even small shifts, such as adjusting a W-4 or earning side income, can change whether you receive a refund or have a balance due.

As shared earlier, for federal returns, the Internal Revenue Service states that most refunds are issued in fewer than 21 calendar days. Filing electronically and choosing direct deposit is the fastest option. Paper returns and mailed checks usually take longer. Most states process refunds within 7 to 21 days, but timelines can vary, and delays do happen depending on state procedures and return details.

Even when a return is filed on time, processing can take longer than expected. Some delays are routine and part of the IRS review process, while others stem from missing or incorrect information. Understanding common causes can help set expectations and reduce frustration.

Common reasons refunds may be delayed include:

Filing early does not always guarantee faster payment if a return needs additional review. Bringing complete and accurate documents to your tax appointment can help reduce the chance of delays.

Owing taxes can feel discouraging, but it is a common outcome. A balance due simply means that not enough tax was paid during the year. This can happen with freelance income, reduced withholding, or changes in credits. Paying by the April deadline (April 15) helps avoid added charges, but owing money does not mean you did something wrong.

If paying your full tax balance at once is not realistic, there are options available. Qualified taxpayers, or an authorized representative with power of attorney, can apply online for a payment plan, also called an installment agreement, to pay the balance over time. These plans allow payments to be spread out in manageable amounts.

Some taxpayers also adjust paycheck withholding or make estimated payments during the year to reduce future balances. Reviewing these options with a tax preparer can help you plan ahead and feel more prepared for the next filing season.