Menu

Your credit score can feel like a mystery. Is it really all that important? Does it matter how high the score is? What if your score is under 700?

The thing is, your credit score is more important than you might realize. And when you apply for a loan for the first time, you’ll see just how important it is to make smart money decisions to protect your score.

That said, whether you're financing a car, paying for furniture, or covering unexpected expenses, installment loans are a common tool to manage costs over time. These loans are paid back in fixed monthly amounts over a set period and can include personal loans, auto loans, and mortgages.

In this article, the team here at Credit Central will explain how installment loans work and how they influence your credit score. We’ll even share some tips to use these loans wisely to build or maintain good credit.

Let’s start by talking about how an installment loan can actually help your credit score. Because believe us, every point your credit score increases, the more it will work in your favor.

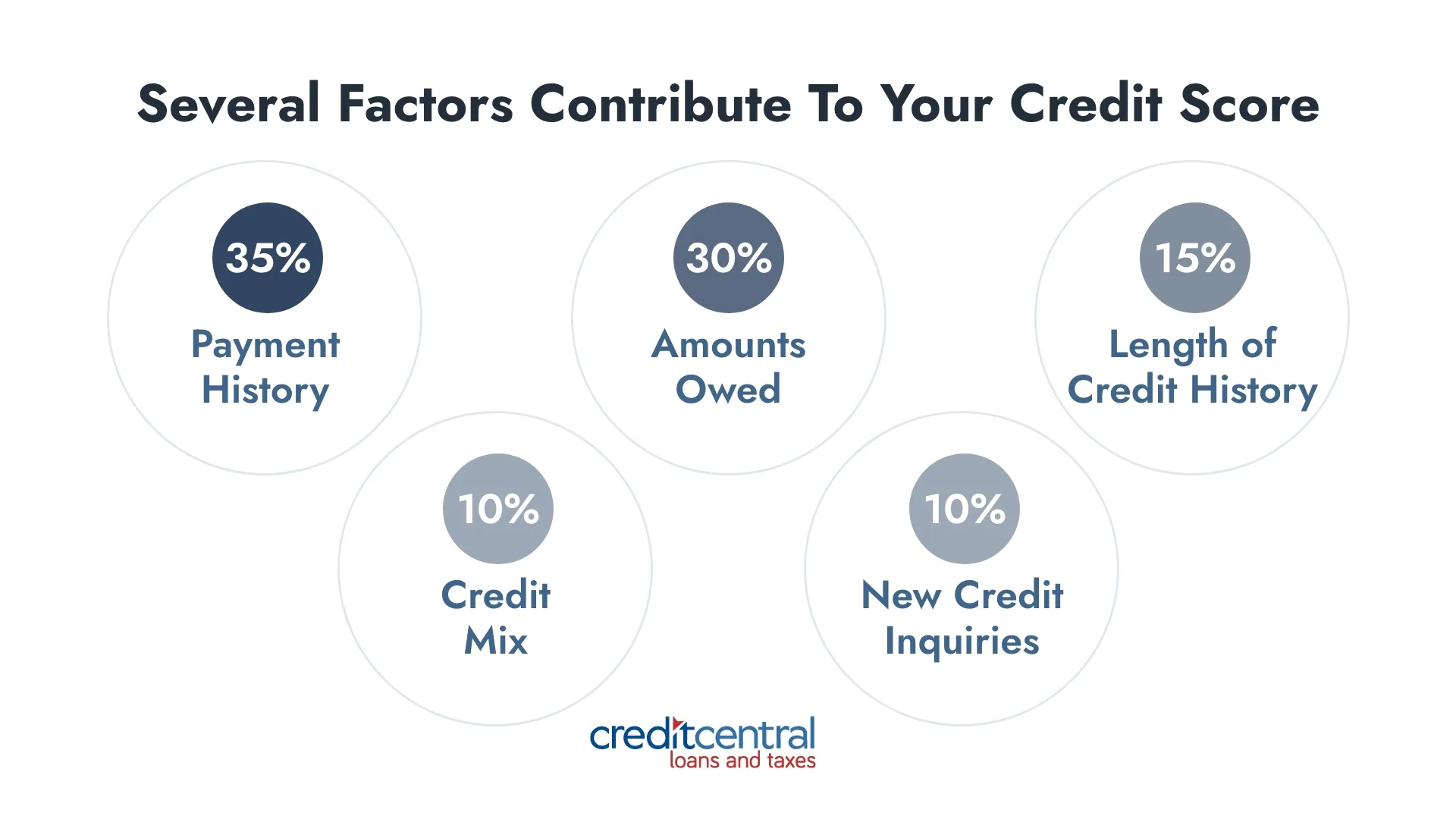

Several factors contribute to your credit score, each with its own weight:

Making consistent, on-time payments on an installment loan directly supports the most important factor: your payment history. It also adds to your credit mix by showing that you can manage different types of credit. If you use the loan to pay off high-interest credit cards, it can lower your credit utilization ratio, which may further improve your score. When used responsibly, installment loans can be a strategic step toward a stronger financial profile.

As with any financial product, there can be a downside. And your credit score is not immune. While installment loans can help build credit, they can also hurt it if not managed carefully.

One of the biggest risks is missed or late payments. According to FICO data, even a single 30-day late payment can lower your score significantly. For someone with a fair credit score, that one late payment could cause a drop of 17 to 37 points. If your score is very good or excellent, the hit is even worse, by 63 to 83 points. And if a payment goes unpaid for 90 days, a fair score could drop 27 to 47 points, while an excellent score might fall by 113 to 133 points. The higher your score, the harder it falls.

Applying for an installment loan also triggers a hard inquiry on your credit report. While not as damaging as a missed payment, it can temporarily lower your score. Hard inquiries can stay on your credit report for up to two years, although most credit-scoring models only weigh those made in the past 12 months.

Lastly, carrying a high loan balance, especially early in the loan term, may signal risk to lenders. It increases your overall debt load, which can affect your ability to take on other credit and may weigh down your score, especially if your income can’t comfortably support the payment.

Thankfully, there are some best practices that you can take to make sure your installment loan works for you, not against you. Here’s what to do.

Installment loans can help or hurt your credit score depending on how you use them. On-time payments, manageable balances, and smart borrowing habits all play a role in keeping your score on track.

At Credit Central, we offer installment loans designed to be simple, straightforward, and budget-friendly. Whether you're looking to cover an unexpected expense or build your credit history, our team is here to help.

Remember, the key is not just borrowing, but borrowing wisely. Let Credit Central be your trusted partner in making smart financial moves. Apply online today.